With Ola Electric’s stock facing a reality check after a period of heightened exuberance, industry experts have expressed concern about the wider euphoria around startup IPOs. Even as a flood of liquidity and positive sentiment has increased investors’ appetite for risk, industry experts remain cautious of Ather’s valuations.

“The current trend of assigning high valuations to early-stage companies raises questions about the sustainability of such pricing,” Vishal Agarwal, partner at Grant Thornton Bharat told Mint. “As capital markets evolve, it’s essential to consider whether these valuations are premature and if companies need to demonstrate more maturity before going public. The true test will be whether their earnings can justify the enthusiasm, a question that only time will answer.”

Can Ather justify a premium valuation?

For Ather, which lags Ola Electric on almost every key financial metric, justifying its possibly high bull-market premium remains an uphill task for now, and it could have a fate similar to Ola Electric, analysts said.

Ola Electric’s shares rose to a high of ₹157.40 after its IPO, 107% over its listing price of ₹76. The stock has since fallen almost 31% to ₹108.94 from its all-time high. The lock-in period for anchor investors also expired during this period, adding 18 crore more shares (4% of the company’s total) for trading and increased the downward pressure on the stock.

Analysts remain sceptical of Ola Electric’s future. Domestic brokerage firm Ambit recently cited increasing competition in the electric two-wheeler industry and a continued focus on market-share expansion over profitability as key downsides for the company going forwards.

Also read: What an IPO signals about Ather’s battle against Ola Electric

Ather’s performance over the past three years has been even worse, raising bigger doubts about its future. But analysts are also taking into account its undisputed product quality, which they believe is a key differentiator between the two rivals.

Hero Motocorp’s almost 40% stake in Ather is also providing some comfort to investors. The marquee motorcycle maker’s decision to not sell its stake during Ather’s IPO is likely to boost investor confidence, analysts said.

Contrasting strategies

Ather’s draft red herring prospectus offers a sobering look at the company’s fundamentals over the past three years. It also highlights the key difference between its business strategy and that of Ola Electric.

Ola Electric’s entry into the electric two-wheeler industry was marked by a strategic acquisition and aggressive expansion of production and distribution. Ather meanwhile took a more tempered and quality-centric approach.

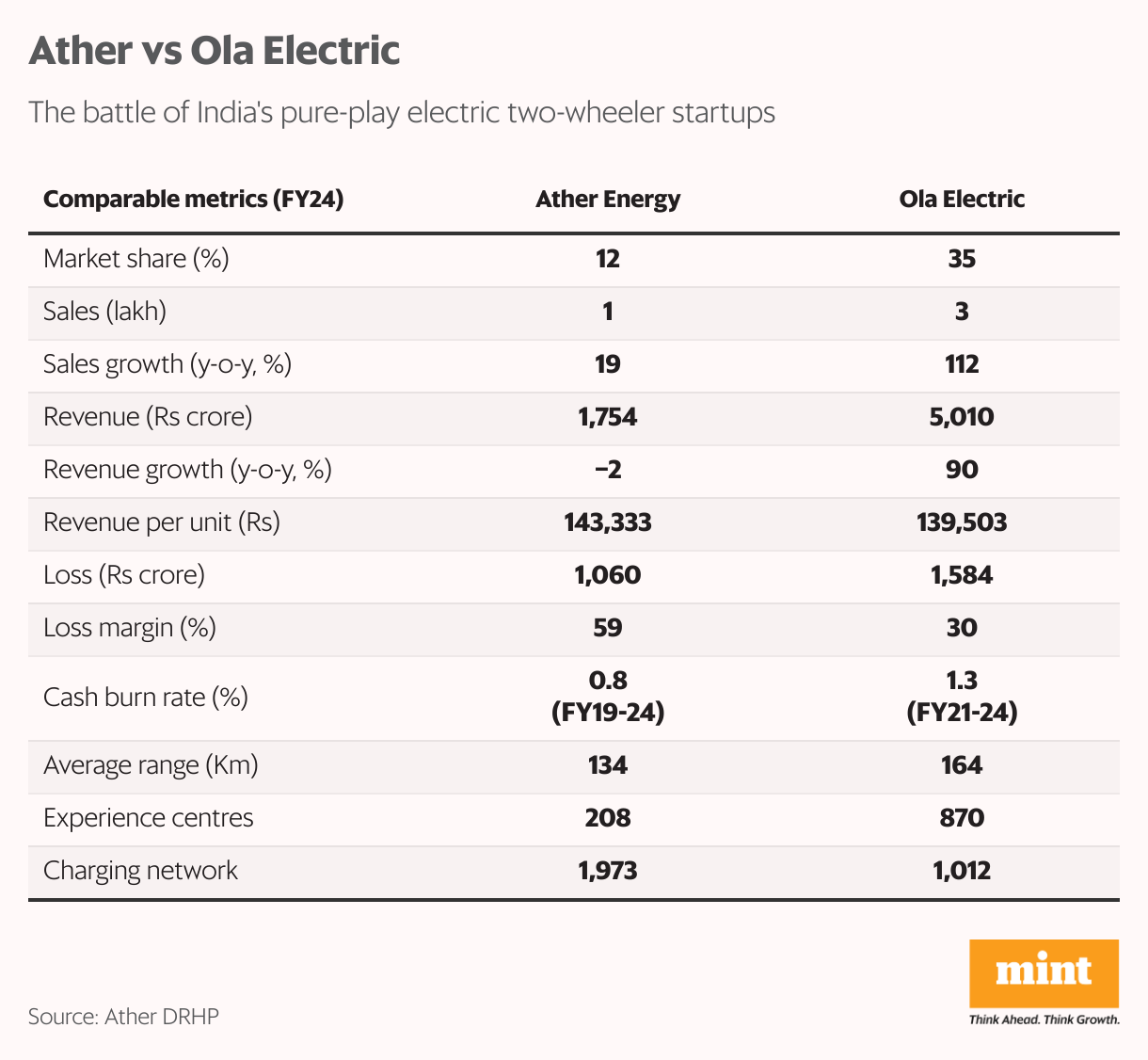

This has caused Ather to lose significant ground to Ola Electric over the past three years, even though its electric two-wheeler journey began much earlier. As of FY24, Ola Electric is the leader with a 35% share of the electric-two-wheeler market, while Ather holds 12%. Ather’s market share grew just 9% year-on-year, while Ola Electric’s grew 67%.

Also read: Ather Energy IPO isn’t as electrifying

“Ola (Electric) set up its factory in record time. It took a very aggressive approach. Fast ramp-up of production and learning on the way was its strategy, while Ather’s approach has been to get the product right first and then ramp up production,” Jay Kale, executive vice president of institutional equity research at Elara Capital told Mint.

Ather’s burn rate over FY19-FY24 was 0.8, while that of Ola Electric over FY21-FY24 was 1.3. This means that Ola Electric spent almost 63% more than Ather in half the time to fuel its aggressive business strategy.

Organic vs inorganic growth

While Ather banked on in-house engineering and built its scooter from scratch, Ola Electric bought out Etergo, a Netherlands-based startup that had a near-production-ready electric scooter to mark its debut. After fortifying its production capacity, Ola Electric rapidly expanded its distribution network.

As of FY24, Ola Electric’s distribution network was four times that of Ather. While Ather had 208 experience centres at the end of FY24, Ola Electric had 870. Most startups are loss-making at first as they look to grow their sales and realise economies of scale as quickly as possible.

Also read: With Rizta, Ather looks to bond better with family scooter market

Ola Electric’s quick takeover as market leader aided its sales volumes significantly. Total sales grew 112% on-year to around three lakh units in FY24, while those of Ather rose only 9% on-year to one lakh units.

Lower sales volume led to a 2% on-year fall in Ather’s revenue to ₹1,754 crore in FY24, whereas Ola Electric’s revenue rose 90% on-year to ₹5,010 crore. Ather had the lowest revenue among its peers in FY24, according to its draft red herring prospectus.

Quality vs quantity

One of the earliest entrants in the electric two-wheeler industry, Ather has been steadfast in perfecting its craft since its inception in 2013. “Ather’s product quality is one of its major differentiating factors amongst peers. Its product quality is probably one of the best in the industry,” Kale said.

A quality- and innovation-based approach led the company to focus primarily on premium, feature-rich electric scooters. As a result, Ather’s revenue per unit has always been higher than Ola Electric’s in the past three years. In FY24, Ather’s revenue per unit was 3% higher than that of Ola Electric’s at ₹1.43 lakh, according to its draft red herring prospectus. Unit economics of the entire electric two-wheeler industry deteriorated in the previous fiscal year as the government reduced its FAME subsidy.

Also read: Electric vehicles become 10% costlier in Delhi, registrations slip

Despite its better unit economics, Ather’s loss rose 24% to ₹1,060 crore in FY24 while that of Ola Electric increased only 8% to ₹1,584 crore. As Ola Electric ramped up its sales volumes by introducing cheaper products, it reduced its loss margin by 43% on-year to 30% in FY24. Ather’s loss margin meanwhile rose 22% on-year to 59%.

“Ather has taken a measured approach in ramping up sales volumes in comparison to Ola (Electric). Perhaps it was a little slower than one would have wanted.”

“Ather has taken a measured approach in ramping up (sales) volumes in comparison to Ola (Electric). Perhaps it was a little slower than one would have wanted,” Kale said. “But now with the launch of Rizta, a family scooter in the convenience segment, it is addressing a wider target audience. With this new product, Ather’s market share should increase going forward.”

The valuation question

Gaining market share requires a combination of increased distribution and production capacity, and competitive pricing to target a large customer base, all of which Ather had been addressing until recently, analysts said.

“These companies have strong business models even though they are yet to become profitable. This is why we saw strong buying interest for Ola (Electric) and probably it will be the same for Ather,” Kranthi Bathini, director of equity strategy at WealthMills Securities told Mint.

Also read: Selfies for subsidies? Govt wants to put its mark on EV discounts

Ather is likely to fetch a valuation of nearly ₹21,000 crore at the upper end of the price band, according to a CNBC-TV18 report. Ola Electric was valued at ₹33,522 crore during its IPO. A 30% discount to Ola Electric’s multiple would mean a valuation of about Rs12,000 crore for Ather, Mint reported recently.

“A flood of liquidity and positive sentiment around the economy have become a lethal combination for India’s ongoing bull market.”

This is significantly lower than the reported number for Ather, which means the promoters are trying to capitalise on the current exuberance in the market by demanding a steep and unsustainable price for their company, analysts said.

“A flood of liquidity and positive sentiment around the economy have become a lethal combination for India’s ongoing bull market,” Bathini said. “Every promoter wants to cash in on the exuberance.”

That said, only time will tell whether Ather’s quality-first strategy works in the long run.