MUMBAI

:

Angel One Ltd gained about 7% in the last two trading sessions following its decision to charge brokerage for cash delivery trades. The Street has cheered the move as the likely gains from the strategy seem enough to offset the impact of true-to-label pricing norms.

The stock price uptick implies that the market doesn’t expect any substantial adverse impact on options volumes owing to the new Security and Exchange Board of India (Sebi) derivative trading norms and that the company is immune to losing customers trading in the cash market to rivals offering free trading.

But such implicit assumptions could be risky.

Angel One has decided to bite the bullet by scrapping the zero-brokerage policy on equity-delivery transactions. It will charge ₹20 per order or 0.1% of the transaction value, whichever is lower, as brokerage on cash-delivery orders. This was on expected lines. Recall that before the introduction of true-to-label pricing norms, the company could earn indirect income in the form of incentives from exchanges on transaction charges. It would collect the transaction charges from all clients at a fixed rate but remit less amount to the exchange based on the discount for total volumes generated, thus pocketing the difference. That route has been closed with the true-to-label pricing.

The company earned ₹110 crore during Q1FY25 as incentives from exchanges, about 10% of its fees and commission income.

Assuming the company can maintain the cash-delivery orders at 60 million, as was the case in Q1FY25, it should be able to earn ₹120 crore to offset the impact of true-to-label pricing. The calculation also assumes a revenue of ₹20 per order and no client loss.

The downside

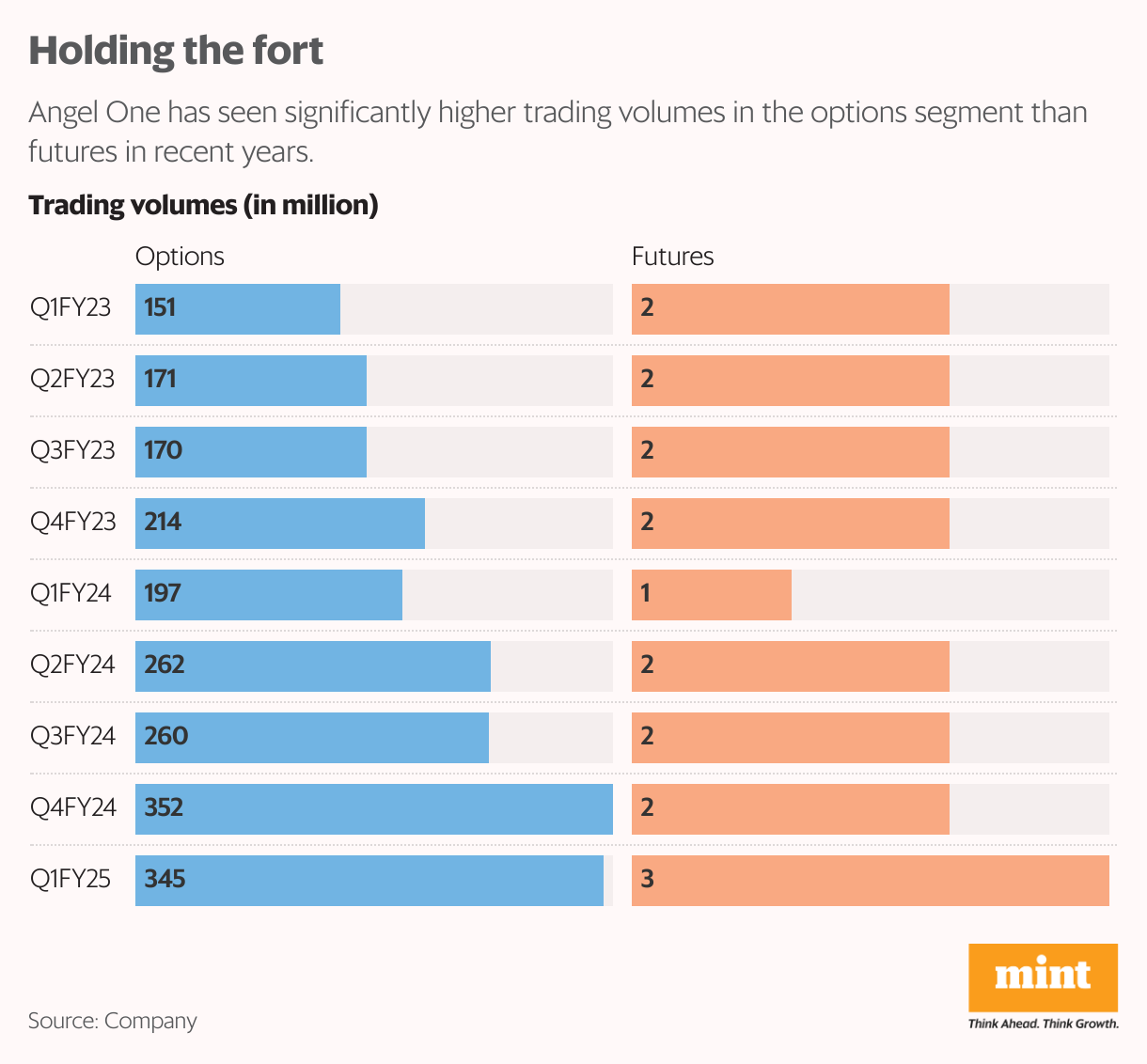

However, options volume could be adversely affected if the activity in F&O declines, especially in options in view of the new Sebi regulations. The most critical regulation is regarding the limitation of one expiry per week per exchange. The weekly expiries introduced in FY19 have been one of the main reasons for the explosion in options trading volume. In Q1FY25, Angel One processed 348 million orders in F&O with 345 million orders in options alone.

Last but not least, Zerodha has refrained from announcing brokerage charges on cash-delivery transactions that are free as of now. Therefore, Angel One also faces a risk of losing clients to the rival. Meanwhile, Angel One stock valuation has come off from the peak of 25x in January to 17x based FY25 Bloomberg consensus earnings per share.